ogc163

Superstar

Getting Rich on Government-Backed Mortgages

A branch manager gets home loans for borrowers with weak credit or low incomes—and taxpayers back him up.

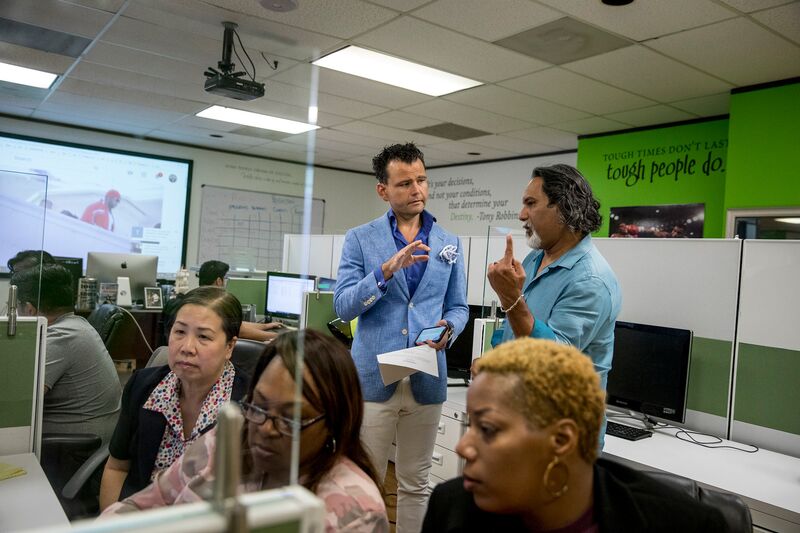

In his corner of American finance, where hard selling meets hard luck, Angelo Christian is a star, and he looks the part. He’s wearing black caiman shoes and a Bordeaux-red silk shirt, tight and open wide at the chest. His dark widow’s peak is slicked high with gel. He has 180,000 Facebook followers and a budding YouTube network, where he shares original videos such as “How to Master Your Mind” and “How to Manage a $50 Million Pipeline.”

Each time Christian sells a home loan, the company he works for, American Financial Network Inc., takes as much as 5 percent—$12,500 on a $250,000 loan, to be distributed among his staff, corporate headquarters, and, of course, himself. As he and his team chase more than 250 leads a week, they’re on pace to close 50 a month. Christian says he has a Lamborghini on order to go with his Mercedes.

On a recent afternoon in a suburban Houston office park, he leans back in his swivel chair, iPhone glued to his cheek. A TV projecting to a screen behind his desk pounds music videos, keeping his adrenaline flowing. He calls back a customer who’s spent hours watching his sales videos: “Bad Credit, I Can Help,” “Fresh Start: Credit Boost,” and “Go For Your Dreams.” This would-be homeowner has a 596 credit score, putting him in the subprime range. His car has been repossessed, something that would likely disqualify him at the Bank of America branch next door.

“Usually a repo that’s like three years old, we’re not really going to sweat that,” he assures the caller. “We’re pretty lenient here.” He steers his prospect to several $400,000 homes with swimming pools. “Have your wife check that out,” he says, referring to a remodeled kitchen with granite countertops. “She’s going to love it.”

Many of Christian’s customers have no savings, poor credit, or low income—sometimes all three. Some are like Joseph Taylor, a corrections officer who saw Christian’s roadside billboard touting zero-down mortgages. Taylor had recently filed for bankruptcy because of his $25,000 in credit card debt. But he just bought his first home for $120,000 with a zero-down loan from Christian’s company. Monthly debt payments now eat up half his take-home pay. “If he can help me, he can help anyone,” Taylor says. “My credit history was just horrible.”

Christian can do this kind of deal because he is, in effect, making the loan on behalf of the federal government through its most important affordable housing program. It’s a sweet deal: He gets his nearly risk-free commission. Taylor puts no money down. If things go south, the government ultimately bears the risk.

This kind of lending echoes the subprime mortgage boom that preceded the credit crisis of 2008. Then, as now, independent mortgage companies, the so-called nonbanks, dominated the business of making loans to people with blemished credit and low incomes. In the pre-crash years, companies such as New Century Financial Corp. helped spur the crisis with their shoddy underwriting standards. Using a line of credit from a major bank, they would offer mortgages essentially to anyone with a pulse. They would then quickly resell them into a market that repackaged them into high-risk securities that were destined for failure, infecting the financial system and requiring a government rescue.

No one is saying the system is close to another collapse. Yet nonbanks, more loosely regulated than the JPMorgan Chases of the world, are bigger players today than during the last mortgage bubble, according to a Brookings Institution report. They’re making almost half of new loans, compared with 19 percent in 2007. As before, many are companies you’ve never heard of, like American Financial Network, a closely held firm based in Brea, Calif. A few are better-known, such as LoanDepot, Freedom Mortgage, and the industry leader, Quicken Loans, with its ubiquitous Rocket Mortgage television commercials.

For first-time purchasers, many nonbank lenders rely on the government’s affordable financing, backed by the Department of Veterans Affairs, the Department of Agriculture, and, most of all, the Federal Housing Administration. Lending under these programs differs in some important ways from the subprime mortgages of the aughts. Unlike the usurious loans of the past, federally backed mortgages can charge low rates—often less than 5 percent—and require documentation of jobs and income. Jonathan Gwin, American Financial Network’s chief operating officer, says delinquencies are low for these kinds of loans. And overall, it’s still difficult for many people to get a mortgage. (Only 3.5 percent of new loans are to people with credit scores below 620, compared with 15 percent in 2007.)

Nonbank mortgages make up about 80 percent of the loans for borrowers insured by the U.S. government. The banks have largely abandoned that market because of tighter scrutiny. As before, lenders use lines of credit to fund the loans, which are packaged into securities—in this case, Ginnie Mae bonds, common in mutual funds and pensions. In the subprime debacle, private investors risked losses if borrowers defaulted. Now, as long as lenders follow the rules for writing loans, the government guarantees FHA mortgages.

To protect taxpayers, FHA borrowers are supposed to make small down payments, equal to 3.5 percent of the home’s purchase price. But many FHA borrowers put nothing down at all. They often get cash from down payment assistance programs, typically run by housing finance agencies or nonprofit groups. The Department of Housing and Urban Development’s inspector general says some of those programs violated HUD rules by having borrowers pay for the assistance in the form of higher rates and fees.

In civil fraud complaints, the Department of Justice has accused many companies, including Quicken and Freedom Mortgage, of improperly underwriting FHA loans and then filing claims for government insurance after borrowers defaulted. In 2016, Freedom Mortgage settled for $113 million, without admitting liability. Quicken is fighting the Justice Department in court. “This is nothing more than a shakedown,” says Quicken Vice Chairman Bill Emerson, who adds that the company makes prudent loans under FHA guidelines. He says multiple state and federal agencies regulate nonbanks.

There are other worrisome signs. Even in a strong economy, recent FHA loans are souring faster than those made years ago when the industry had stricter credit standards, the Mortgage Bankers Association says. About 9 percent are 30 days or more past due, manageable by historical standards and well below the high of 14 percent in 2009. But the FHA itself is concerned that, on average, borrowers are spending 43 percent of their income on debt payments, the highest level in at least two decades.

A branch manager gets home loans for borrowers with weak credit or low incomes—and taxpayers back him up.

In his corner of American finance, where hard selling meets hard luck, Angelo Christian is a star, and he looks the part. He’s wearing black caiman shoes and a Bordeaux-red silk shirt, tight and open wide at the chest. His dark widow’s peak is slicked high with gel. He has 180,000 Facebook followers and a budding YouTube network, where he shares original videos such as “How to Master Your Mind” and “How to Manage a $50 Million Pipeline.”

Each time Christian sells a home loan, the company he works for, American Financial Network Inc., takes as much as 5 percent—$12,500 on a $250,000 loan, to be distributed among his staff, corporate headquarters, and, of course, himself. As he and his team chase more than 250 leads a week, they’re on pace to close 50 a month. Christian says he has a Lamborghini on order to go with his Mercedes.

On a recent afternoon in a suburban Houston office park, he leans back in his swivel chair, iPhone glued to his cheek. A TV projecting to a screen behind his desk pounds music videos, keeping his adrenaline flowing. He calls back a customer who’s spent hours watching his sales videos: “Bad Credit, I Can Help,” “Fresh Start: Credit Boost,” and “Go For Your Dreams.” This would-be homeowner has a 596 credit score, putting him in the subprime range. His car has been repossessed, something that would likely disqualify him at the Bank of America branch next door.

“Usually a repo that’s like three years old, we’re not really going to sweat that,” he assures the caller. “We’re pretty lenient here.” He steers his prospect to several $400,000 homes with swimming pools. “Have your wife check that out,” he says, referring to a remodeled kitchen with granite countertops. “She’s going to love it.”

Many of Christian’s customers have no savings, poor credit, or low income—sometimes all three. Some are like Joseph Taylor, a corrections officer who saw Christian’s roadside billboard touting zero-down mortgages. Taylor had recently filed for bankruptcy because of his $25,000 in credit card debt. But he just bought his first home for $120,000 with a zero-down loan from Christian’s company. Monthly debt payments now eat up half his take-home pay. “If he can help me, he can help anyone,” Taylor says. “My credit history was just horrible.”

Christian can do this kind of deal because he is, in effect, making the loan on behalf of the federal government through its most important affordable housing program. It’s a sweet deal: He gets his nearly risk-free commission. Taylor puts no money down. If things go south, the government ultimately bears the risk.

This kind of lending echoes the subprime mortgage boom that preceded the credit crisis of 2008. Then, as now, independent mortgage companies, the so-called nonbanks, dominated the business of making loans to people with blemished credit and low incomes. In the pre-crash years, companies such as New Century Financial Corp. helped spur the crisis with their shoddy underwriting standards. Using a line of credit from a major bank, they would offer mortgages essentially to anyone with a pulse. They would then quickly resell them into a market that repackaged them into high-risk securities that were destined for failure, infecting the financial system and requiring a government rescue.

No one is saying the system is close to another collapse. Yet nonbanks, more loosely regulated than the JPMorgan Chases of the world, are bigger players today than during the last mortgage bubble, according to a Brookings Institution report. They’re making almost half of new loans, compared with 19 percent in 2007. As before, many are companies you’ve never heard of, like American Financial Network, a closely held firm based in Brea, Calif. A few are better-known, such as LoanDepot, Freedom Mortgage, and the industry leader, Quicken Loans, with its ubiquitous Rocket Mortgage television commercials.

For first-time purchasers, many nonbank lenders rely on the government’s affordable financing, backed by the Department of Veterans Affairs, the Department of Agriculture, and, most of all, the Federal Housing Administration. Lending under these programs differs in some important ways from the subprime mortgages of the aughts. Unlike the usurious loans of the past, federally backed mortgages can charge low rates—often less than 5 percent—and require documentation of jobs and income. Jonathan Gwin, American Financial Network’s chief operating officer, says delinquencies are low for these kinds of loans. And overall, it’s still difficult for many people to get a mortgage. (Only 3.5 percent of new loans are to people with credit scores below 620, compared with 15 percent in 2007.)

Nonbank mortgages make up about 80 percent of the loans for borrowers insured by the U.S. government. The banks have largely abandoned that market because of tighter scrutiny. As before, lenders use lines of credit to fund the loans, which are packaged into securities—in this case, Ginnie Mae bonds, common in mutual funds and pensions. In the subprime debacle, private investors risked losses if borrowers defaulted. Now, as long as lenders follow the rules for writing loans, the government guarantees FHA mortgages.

To protect taxpayers, FHA borrowers are supposed to make small down payments, equal to 3.5 percent of the home’s purchase price. But many FHA borrowers put nothing down at all. They often get cash from down payment assistance programs, typically run by housing finance agencies or nonprofit groups. The Department of Housing and Urban Development’s inspector general says some of those programs violated HUD rules by having borrowers pay for the assistance in the form of higher rates and fees.

In civil fraud complaints, the Department of Justice has accused many companies, including Quicken and Freedom Mortgage, of improperly underwriting FHA loans and then filing claims for government insurance after borrowers defaulted. In 2016, Freedom Mortgage settled for $113 million, without admitting liability. Quicken is fighting the Justice Department in court. “This is nothing more than a shakedown,” says Quicken Vice Chairman Bill Emerson, who adds that the company makes prudent loans under FHA guidelines. He says multiple state and federal agencies regulate nonbanks.

There are other worrisome signs. Even in a strong economy, recent FHA loans are souring faster than those made years ago when the industry had stricter credit standards, the Mortgage Bankers Association says. About 9 percent are 30 days or more past due, manageable by historical standards and well below the high of 14 percent in 2009. But the FHA itself is concerned that, on average, borrowers are spending 43 percent of their income on debt payments, the highest level in at least two decades.